You’ve found the perfect piece of equipment to scale your business. It’s exactly what you need to serve more customers, increase productivity, or improve your operations. There’s just one problem: the sticker price. Buying equipment outright without proper equipment financing can drain your cash reserves, leaving you vulnerable if an emergency hits or an unexpected opportunity emerges.

This is where equipment financing comes in. Instead of depleting your working capital with a lump-sum purchase, equipment financing lets you spread the cost over time with predictable monthly payments. You get the equipment you need today, preserve cash for operations and growth, and build your business credit along the way.

Whether you run a restaurant, manage a construction crew, operate a trucking fleet, or manufacture products, equipment financing adapts to your industry and budget. This guide walks you through everything you need to know about equipment financing—from how it works to comparing your options to understanding the costs and benefits specific to your business type.

By the end, you’ll understand which equipment financing solution fits your situation, how to qualify, and how to move forward with confidence.

What Is Equipment Financing?

Equipment financing is a secured loan that lets you purchase or lease business equipment without paying the full cost upfront. The lender provides the funds to buy the equipment, and you repay the loan over a set period—typically two to seven years—with interest and fees added to your monthly payment.

The key distinction: the equipment itself serves as collateral for the loan. This means the lender has legal rights to the equipment if you default on payments. Because of this security, equipment financing generally carries lower interest rates than unsecured loans, making it a cost-effective way to acquire the tools your business needs.

What Qualifies as Equipment?

Nearly any business asset with a useful lifespan of more than one year can be financed. Common examples include:

- Food service: Commercial ovens, refrigeration units, fryers, POS systems, ice machines

- Construction: Excavators, skid steers, cranes, nail guns, compressors, scaffolding

- Transportation: Semi trucks, trailers, forklifts, delivery vans

- Manufacturing: CNC machines, production lines, welding equipment, hydraulic presses

- Medical/Dental: Imaging equipment, surgical chairs, sterilizers, diagnostic tools

- Agriculture: Tractors, harvesters, irrigation systems, grain storage

- Retail: Checkout systems, displays, shelving, security systems

Equipment financing does NOT typically cover inventory, accounts receivable, real estate, or intangible assets like patents or software licenses.

Equipment Financing vs. Equipment Leasing

While both allow you to use equipment without buying outright, they work differently:

Equipment Financing: You’re taking out a loan to purchase equipment. You own it after the loan is paid off. You’re responsible for maintenance, insurance, and repairs. You can depreciate the equipment on your taxes and claim Section 179 deductions.

Equipment Leasing: You’re renting equipment for a predetermined period. The lessor owns it and typically handles maintenance. At the end of the lease, you return the equipment. Lease payments are fully tax-deductible as operating expenses. You have no asset at the end.

The right choice depends on your situation—we’ll dive deeper into this comparison later.

How Does Equipment Financing Work?

Equipment financing follows a straightforward process from application to acquisition to repayment. Understanding the steps helps you prepare and know what to expect.

The Equipment Financing Process

Step 1: Application & Prequalification (1-2 hours)

You complete an online application with basic information about your business, how long you’ve been operating, your credit, and the equipment you want to finance. Many lenders, including LendWiz, provide instant prequalification without a hard credit pull—meaning your credit score isn’t affected.

Step 2: Lender Review & Underwriting (24-48 hours)

The lender reviews your application, verifies your information, and pulls your credit report. They examine your business financials, personal credit history, time in business, and annual revenue. For small businesses, they often review bank statements and tax returns from the past 1-2 years.

Step 3: Approval & Offer (1-2 business days)

If approved, you receive a loan offer detailing:

- Loan amount (how much you can borrow)

- Interest rate (APR)

- Term length (12-84 months typically)

- Monthly payment

- Down payment requirement (if any)

- Fees (origination, document, lien registration)

Step 4: Equipment Selection & Verification (1-5 days)

You finalize which equipment you’re purchasing and provide the lender with specifications, quotes, or invoices. The lender verifies the equipment’s value and condition.

Step 5: Loan Documentation & Signing (1-3 business days)

You sign the loan agreement, equipment specification sheet, UCC-1 financing statement (which gives the lender a legal claim to the equipment), and other required documents. This can typically be done electronically.

Step 6: Funding & Purchase (3-7 business days)

The lender funds the loan. Many lenders will pay the equipment vendor directly, though some fund your business account and you handle the purchase. Either way, you receive the equipment.

Step 7: Repayment (Monthly for 2-7 years)

You make fixed monthly payments. Your payment includes principal, interest, and any loan fees. Payments are consistent every month, making budgeting simple and predictable.

Equipment as Collateral

Throughout the loan term, the equipment remains pledged as collateral. The lender files a UCC-1 financing statement, which is a public record showing they have a legal interest in the equipment. This protects the lender if you default—they can repossess and sell the equipment to recoup their losses.

However, for your business, this is a benefit. Because the equipment serves as collateral, the lender takes on less risk, which means you get better rates and terms than you would with an unsecured loan.

Timeline Reality

From application to equipment delivery, budget 7-14 business days under normal circumstances. Some lenders move faster (LendWiz typically approves qualifying applications in 24-48 hours), while others may take longer. If you need equipment urgently, choose a lender known for speed and have all your documentation ready to go.

Types of Equipment Financing

There isn’t a one-size-fits-all approach to equipment financing. Depending on your credit, industry, timeline, and preferences, you have several options to choose from.

Equipment Loans (Traditional)

A traditional equipment loan is a straightforward secured loan where you borrow money to purchase equipment and repay it over a fixed term—typically 3-5 years, though terms can extend to 7 years for larger purchases.

How it works: You apply, get approved, receive funds, buy the equipment, and pay back the loan with fixed monthly payments. You own the equipment from day one (subject to the lender’s lien).

Best for: Businesses that plan to keep and use equipment long-term, want to own an asset, and have decent credit (670+).

Pros:

- Own the equipment outright after loan payoff

- Can depreciate the asset on taxes

- Fixed payments make budgeting easy

- No mileage or usage restrictions

Cons:

- You handle all maintenance and repairs

- You’re responsible for insurance

- Equipment ages and becomes less valuable

- Higher upfront commitment

Typical rates: 8-25% APR depending on credit, industry, and down payment

Equipment Leasing

With equipment leasing, you rent equipment from a lessor for a predetermined period (typically 24-60 months). You make monthly lease payments and return the equipment at the end.

How it works: You apply to lease, get approved, receive the equipment, make monthly payments, and return it when the lease ends. Some leases include maintenance; others don’t.

Best for: Businesses that want the latest equipment, don’t want ownership responsibilities, or prefer flexibility to upgrade frequently.

Pros:

- Lower monthly payments than loans

- Lessor typically handles maintenance

- Easy to upgrade to newer equipment

- Full lease payments are tax-deductible

- Predictable costs

Cons:

- You never own the asset

- You’re liable for damage beyond normal wear and tear

- Mileage/usage restrictions may apply

- Early termination penalties

Typical rates: 5-15% effective cost (varies by equipment type)

Equipment Line of Credit

An equipment line of credit is a revolving credit facility that allows you to draw funds to purchase equipment as needed, up to your approved limit. You only pay interest on the amount you’ve drawn.

How it works: You’re approved for a limit (e.g., $100,000). As you need equipment, you draw funds, purchase equipment, and repay that draw over time. When you’ve repaid the draw, those funds become available again.

Best for: Growing businesses that purchase equipment in stages or on an ongoing basis.

Pros:

- Flexibility to draw funds as needed

- Only pay interest on what you use

- Reusable—pay down a draw and redraw later

- Faster than applying for individual loans

Cons:

- Variable interest rates possible

- May require periodic review/renewal

- Requires good credit

- More complex accounting

Typical rates: 10-25% APR depending on creditworthiness

SBA Equipment Loans

The Small Business Administration (SBA) partners with banks and lenders to guarantee loans for small businesses. Equipment financing qualifies as a supported use.

How it works: You apply through an SBA-certified lender. The SBA guarantees a portion of the loan (typically 85%), which reduces the lender’s risk and lets them offer better terms. You repay the loan directly.

Best for: Established businesses (typically 2+ years in operation) that struggle to qualify for traditional financing.

Pros:

- Lower interest rates (often 1-3 points below market)

- Longer terms (up to 10 years for equipment)

- More flexible credit requirements

- Lenders more willing to work with seasonal or declining sales

Cons:

- Longer approval timeline (30-60 days)

- More extensive documentation required

- SBA guarantee fees (typically 3%)

- Personal guarantee required

Typical rates: 7-15% APR depending on prime rate and lender

Learn more: Visit SBA.gov for resources and lender search tools.

Vendor Financing

Some equipment manufacturers and dealers offer in-house financing, allowing you to finance your purchase directly through them rather than through a bank or alternative lender.

How it works: You buy equipment from the vendor, and instead of paying upfront, the vendor extends credit. You make payments to the vendor (or their finance partner) over time.

Best for: Startups or businesses with poor credit that can’t qualify elsewhere; larger purchases where the vendor can absorb some risk.

Pros:

- May approve when banks won’t

- Streamlined process

- Sometimes offered at promotional rates

- Vendor may work with you on terms

Cons:

- Often higher interest rates than bank loans

- Limited to equipment from that vendor

- Fewer consumer protections

- May require larger down payment

Typical rates: 12-30%+ APR

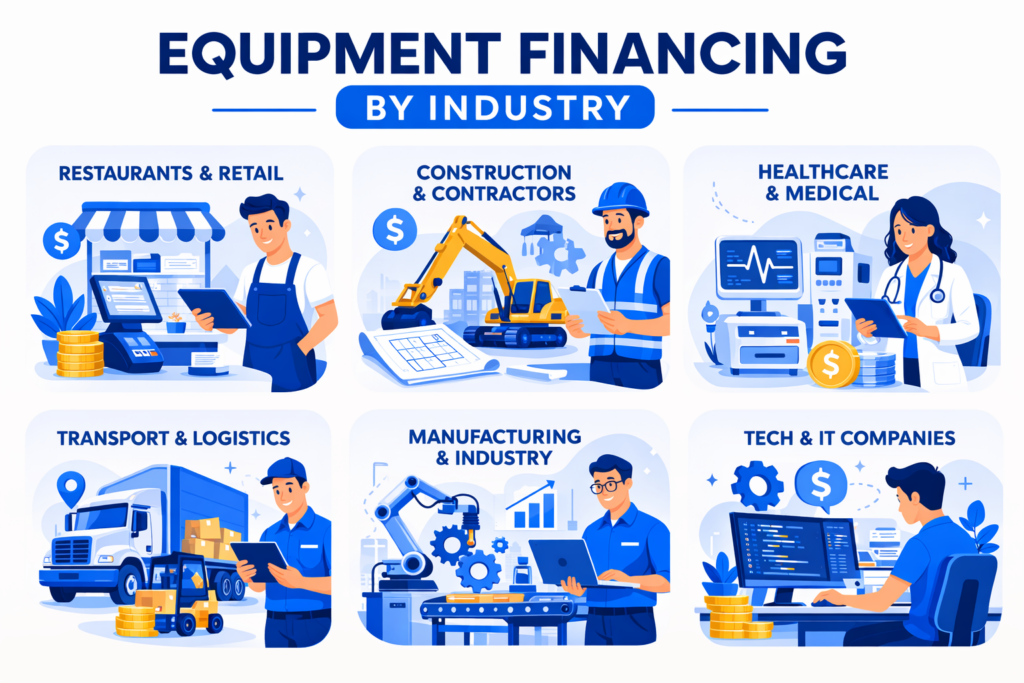

Equipment Financing by Industry

Equipment financing isn’t one-size-fits-all because equipment costs, useful life, and financing challenges vary dramatically by industry. Let’s explore how equipment financing works for specific business types.

Restaurant Equipment Financing

Restaurants have some of the highest equipment costs among small businesses. A full kitchen setup can easily run $50,000-$150,000, and that’s before you buy dining furniture, POS systems, or exterior signage.

Common equipment:

- Commercial ovens ($2,000-$8,000)

- Refrigeration (reach-in coolers, walk-ins: $3,000-$12,000)

- Grills and fryers ($1,500-$4,000)

- POS systems ($3,000-$10,000)

- Dishwashers ($2,500-$5,000)

Financing benefits: Equipment financing lets you open your restaurant or upgrade your kitchen without decimating working capital. You preserve cash to stock food inventory, cover initial payroll, and handle the inevitable startup surprises.

Typical terms: 3-5 years; rates 10-20% APR

Pro tip: New restaurants often qualify for vendor financing from equipment suppliers, sometimes at promotional rates if you commit to multiple purchases.

Construction Equipment Financing

Construction businesses operate on tight margins and heavy equipment is capital-intensive. A single excavator costs $30,000-$80,000; a crane, $50,000-$200,000+.

Common equipment:

- Excavators and skid steers ($25,000-$80,000)

- Cranes and lifts ($40,000-$250,000)

- Compressors and generators ($5,000-$15,000)

- Concrete and asphalt tools ($10,000-$50,000)

- Scaffolding systems ($15,000-$40,000)

Financing benefits: Equipment financing lets you take on larger projects without owning all the equipment outright. You can match equipment purchases to project timelines. Many construction lenders understand seasonal cash flow fluctuations.

Typical terms: 3-7 years; rates 9-18% APR

Pro tip: Construction businesses with strong project pipelines can qualify for larger loans and better rates. Document project contracts and backlog when applying.

Trucking & Transportation Equipment Financing

Semi trucks represent the biggest asset most trucking companies will finance. A new semi truck runs $80,000-$150,000; used models, $30,000-$80,000. Trailers add another $15,000-$40,000.

Common equipment:

- Semi trucks (tractor units: $80,000-$150,000)

- Trailers (dry vans, refrigerated, flatbeds: $15,000-$40,000)

- Specialized trailers (tankers, lowbeds: $30,000-$60,000)

- Forklifts and dock equipment ($10,000-$30,000)

- Telematics and safety systems ($500-$2,000 per vehicle)

Financing benefits: Equipment financing makes it possible to grow your fleet without massive capital outlays. Many trucking lenders allow you to finance multiple vehicles under one credit facility.

Typical terms: 3-7 years; rates 8-16% APR (used trucks cost more)

Pro tip: Your credit score, driving record, and load history all matter. Consistent on-time payment history with factoring companies or previous lenders significantly improves your rates.

Manufacturing Equipment Financing

Manufacturing equipment is expensive and specialized. A used CNC machine costs $20,000-$100,000+; new production lines can exceed $500,000.

Common equipment:

- CNC machines and machining centers ($20,000-$150,000)

- Production lines and automation ($50,000-$500,000+)

- Welding equipment ($5,000-$30,000)

- Hydraulic and pneumatic systems ($10,000-$50,000)

- Quality control and testing equipment ($10,000-$100,000)

Financing benefits: Equipment financing spreads the cost of modernization across years when the equipment generates revenue. Many manufacturers can finance used or refurbished equipment through specialized lenders.

Typical terms: 3-5 years for used equipment; 5-7 years for new; rates 9-18% APR

Pro tip: Refurbished and used equipment often qualifies for financing at better rates than new. Get an independent appraisal to support valuations.

Medical & Dental Equipment

Medical and dental practices require expensive, specialized equipment. A dental chair runs $3,000-$8,000; diagnostic imaging equipment, $50,000-$500,000+.

Common equipment:

- Dental chairs and operatory units ($3,000-$8,000 each)

- X-ray and imaging systems ($10,000-$100,000)

- Surgical equipment and sterilizers ($5,000-$30,000)

- HVAC and air quality systems ($10,000-$50,000)

- IT and EMR systems ($5,000-$25,000)

Financing benefits: Medical professionals can finance equipment with predictable repayment schedules that align with patient revenue. Many healthcare-focused lenders understand practice finances.

Typical terms: 3-5 years; rates 8-15% APR

Pro tip: Established practices with 2+ years of operation and strong personal credit (700+) receive the best rates.

Equipment Financing Rates, Terms & Costs

Understanding what you’ll actually pay is crucial to evaluating equipment financing options. Rates, terms, and fees vary significantly based on multiple factors.

Typical Rate Ranges

Equipment financing rates vary by lender, your credit score, the equipment type, industry, loan amount, and down payment:

| Financing Type | Typical APR | Key Factors |

|---|---|---|

| Traditional Equipment Loan (Good Credit) | 8-15% | Credit score 700+, established business, 20-30% down |

| Traditional Equipment Loan (Fair Credit) | 15-22% | Credit score 600-699, newer business |

| Equipment Lease | 5-12% (effective) | Based on equipment type and lessor |

| Equipment Line of Credit | 12-25% | Based on creditworthiness, revolving nature |

| SBA Equipment Loan | 7-14% | Lower due to federal guarantee |

| Vendor Financing | 12-30%+ | Often higher; limited alternatives |

What impacts your rate:

- Credit score: 50-100+ basis points difference between 650 and 750+

- Business credit: Established business credit history improves rates

- Time in business: 2+ years gets better rates than startups

- Industry risk: Some industries have higher rates due to asset risk

- Loan amount: Larger loans sometimes carry lower rates

- Down payment: 20-30% down significantly improves your offer

- Equipment age: New equipment qualifies for better rates than used

- Equipment type: Stable-value equipment (trucks) vs. rapidly depreciating (computers)

Loan Terms (Duration)

Equipment financing terms typically range from 24-84 months:

- 24-36 months: Shorter term, higher monthly payment, less total interest paid. Good for lower-cost equipment or strong cash flow.

- 48-60 months: Sweet spot for most businesses. Balances monthly payment affordability with reasonable total interest.

- 60-84 months: Lower monthly payment, higher total interest paid. Useful when equipment has longer useful life or cash flow is tight.

Pro tip: SBA loans offer up to 120 months for equipment, allowing extremely low monthly payments for established businesses willing to extend repayment.

Down Payment Expectations

Down payments typically range from 0-30%:

- 0-10% down: Available to strong credit (700+) and established businesses; rare for startups

- 10-20% down: Standard requirement; what most lenders expect

- 20-30% down: Improves your rate and approval odds, especially with fair credit

- 30%+ down: Maximizes approval odds and gets best pricing

Down payment reduces the amount financed, which reduces lender risk and improves your rate.

Fee Structures

Beyond interest, expect these costs:

- Origination fee: 1-5% of loan amount (origination cost)

- Documentation/processing fee: $250-$1,000 (covers paperwork and verification)

- UCC filing fee: $50-$200 (lender’s legal claim to equipment)

- Appraisal fee: $0-$500 if equipment needs independent valuation

- Insurance: You typically buy equipment insurance; lender may require proof

Some lenders build fees into your APR; others charge separately. Always ask for a complete breakdown before accepting an offer.

Rate Comparison by Financing Type

Here’s what a $30,000 equipment purchase looks like across different financing methods:

| Financing Type | Interest Rate | Down Payment | Monthly Payment (60 mo.) | Total Cost | Time to Approve |

|---|---|---|---|---|---|

| Traditional Loan (Good Credit) | 12% APR | $6,000 | $508 | $36,480 | 2-3 days |

| SBA Equipment Loan | 9.5% APR | $3,000 | $504 | $33,240 | 30-45 days |

| Equipment Lease | 8% effective | $0 | $425 | $25,500* | 2-3 days |

| Vendor Financing | 16% APR | $3,000 | $570 | $38,200 | 1-2 days |

| Equipment Line of Credit | 18% APR | $6,000 | $532 | $37,920 | 3-5 days |

*Lease total is cost only; you don’t own equipment at end

The savings from a lower rate add up fast. A 3-point rate reduction on a $30,000 loan saves you roughly $2,700 over five years.

Requirements to Qualify

Equipment financing requirements are less stringent than traditional bank loans, but lenders still evaluate several factors to determine if they’ll approve you and at what rate.

Credit Score

Credit score is one of the first things a lender evaluates:

- 700+: Excellent. You’ll receive the best rates and terms. Most lenders auto-approve in this range.

- 650-699: Good. Typical approval range. You’ll get decent rates, but expect standard documentation requirements.

- 600-649: Fair. You’ll likely get approved, but rates may be 3-5 points higher. Some alternative lenders specialize here.

- Below 600: Challenging. Many traditional lenders won’t approve; you may need SBA loans, vendor financing, or specialized equipment lenders. Rates will be higher.

Important: Many lenders offer prequalification without a hard credit pull. Checking your prequalification status doesn’t hurt your score.

Business Requirements

Beyond your credit, lenders evaluate:

- Time in business: Most lenders require 6 months to 2 years in operation. Startups can qualify through SBA loans or vendor financing, though with fewer options.

- Annual revenue: Lenders typically want to see $50,000-$100,000+ annual revenue, though requirements vary. Some lenders work with newer or smaller businesses.

- Business credit score: If you’ve established business credit, this helps. It’s not required, but it strengthens your application.

- Business structure: Sole proprietorships, LLCs, S-Corps, and C-Corps all qualify. You’ll simply need to provide different documentation.

Personal Finances

Your personal financial situation matters, especially for small businesses:

- Personal credit score: Usually weighted 40-60% in the approval decision

- Personal income: If business income is low, personal income helps (W-2 income, rental income, investment income)

- Personal credit history: Late payments, collections, or bankruptcies hurt, but aren’t automatic disqualifiers

- Personal guarantees: Lenders almost always require you personally guarantee the business loan

Documentation Needed

Have these documents ready:

Business Documents:

- Business license or articles of incorporation

- Recent business bank statements (last 2-3 months)

- Business tax returns (last 1-2 years)

- Profit & loss statement (if available)

- Business plan (optional but helpful for startups)

Personal Documents:

- Personal ID (driver’s license)

- Personal tax returns (last 2 years, especially if business shows low income)

- Personal bank statements (may be requested)

- Proof of personal income (W-2s, 1099s, or pay stubs)

Equipment Documents:

- Equipment quotes or invoices

- Equipment specifications

- Photos (for used equipment)

- Proof of purchase location

What Improves Your Chances

- Larger down payment: 20-30% down signals commitment and reduces lender risk

- Shorter loan term: Requesting 3-4 years instead of 7 shows stronger cash flow

- Business cash flow: Demonstrating consistent, growing revenue helps tremendously

- Collateral: If you can pledge additional collateral (business assets, real estate), your approval odds improve

- Personal financial strength: High personal savings, investments, or home equity help

- Business owner experience: Owners with relevant industry experience get better terms

Equipment Financing vs. Leasing: Which Is Better?

Should you finance equipment or lease it? The answer depends on your business model, cash flow, and long-term goals. Let’s break down the decision.

Side-by-Side Comparison

| Aspect | Equipment Financing | Equipment Leasing |

|---|---|---|

| Ownership | You own the equipment | Lessor owns; you use it |

| Upfront Cost | Down payment (10-30%) | Often $0 down |

| Monthly Payment | Loan payment | Lease payment |

| Payment Duration | 24-84 months | 24-60 months |

| Maintenance | You handle all maintenance | Often included in lease |

| Technology/Upgrades | You own outdated equipment | Easy to upgrade to new models |

| Tax Benefits | Depreciation + Section 179 | 100% lease payment deductible |

| Mileage/Usage Restrictions | None | May apply |

| Residual Value Risk | You own it after payoff | Lessor bears this risk |

| Early Termination | Can’t easily exit | Early termination fees |

| Total Cost (5 years) | Usually lower long-term | Usually higher but includes service |

Ownership Considerations

Equipment Financing = Ownership

When you finance equipment, you own it once the loan is paid off. This means:

- You control what happens to the equipment

- You can sell it, trade it, or keep it for years

- You bear the risk if it becomes obsolete

- You’re responsible if it breaks or needs repair

- You have an asset on your balance sheet

Equipment Leasing = Usage Rights

When you lease, you’re renting equipment for a set period. You:

- Return the equipment at lease end

- Don’t own an asset

- Have predictable costs (lease payments, maintenance)

- Can upgrade to newer equipment every few years

- Avoid technology obsolescence risk

Tax Implications: Section 179 & Cost Segregation

Equipment financing offers significant tax advantages that leasing doesn’t provide.

Section 179 Deduction (Equipment Financing)

Section 179 of the tax code allows you to deduct the full purchase price of equipment in the year you buy it, rather than depreciating it over several years. For 2026, the Section 179 limit is $1.36 million (this changes yearly).

Example: You finance a $40,000 commercial oven. Using Section 179, you can deduct the full $40,000 in your first year, reducing your taxable income by $40,000 and potentially saving $9,200-$13,600 in taxes (depending on your tax bracket).

Bonus Depreciation (Equipment Financing)

If you hit Section 179 limits, bonus depreciation allows 100% depreciation in year one for qualified equipment purchases.

Regular Depreciation (Equipment Financing)

Equipment is typically depreciated over 5-7 years using MACRS (Modified Accelerated Cost Recovery System). You deduct a portion each year.

Lease Payments (Equipment Leasing)

With a lease, 100% of lease payments are deductible as business expenses. However, you don’t own the equipment, so you don’t get Section 179 or depreciation benefits.

Tax Bottom Line: Equipment financing typically saves more in taxes for equipment under $1.36 million due to Section 179. However, consult your CPA because tax situations vary.

When Equipment Financing Makes Sense

- You plan to keep equipment long-term (5+ years)

- Equipment won’t become obsolete quickly (industrial equipment, trucks)

- You want an asset on your balance sheet

- You want to maximize tax deductions through Section 179

- You want to build business credit

- Equipment has stable resale value

When Equipment Leasing Makes Sense

- You want the latest technology (computers, servers, diagnostic equipment)

- Equipment becomes outdated quickly

- You want to avoid maintenance responsibility

- You want lower monthly payments

- You want flexibility to upgrade or exit

- You have inconsistent equipment needs

- Your industry sees rapid equipment evolution

Benefits of Equipment Financing

Beyond simply getting the equipment you need, equipment financing offers substantial business benefits.

Preserve Working Capital

The most immediate benefit: you don’t drain your cash reserves. Instead of writing a $50,000 check for restaurant equipment, you preserve that cash for:

- Inventory and supplies

- Payroll and staffing

- Marketing and customer acquisition

- Emergency reserves

- Unexpected opportunities

This liquidity is crucial for small businesses where every dollar matters.

Tax Advantages (Section 179 Deduction)

As discussed, equipment financing unlocks Section 179 deductions. If you finance $50,000 in equipment, you might save $12,500-$17,500 in taxes in year one. This can offset the cost of financing.

Flexible Terms

Lenders understand that different equipment has different useful lives. You can match your loan term to how long you’ll actually use the equipment:

- Quick-turnover equipment: 24-36 month term

- Stable equipment: 48-60 month term

- Long-life equipment: 60-84 month term

This flexibility ensures your monthly payment aligns with equipment value and your cash flow.

Build Business Credit

Equipment financing reports to business credit bureaus (Dun & Bradstreet, Experian Business, Equifax Business). Prompt payments build your business credit score, which helps you:

- Qualify for larger loans in the future

- Get better rates on future financing

- Qualify for business credit cards

- Build credibility with vendors and suppliers

Get Newer, Better Equipment

Rather than buying whatever used equipment you can afford, financing lets you purchase the right equipment for your needs:

- More efficient models that reduce operating costs

- Equipment with newer features that improve quality

- Equipment with better warranties

- Models with longer useful lives

Better equipment often means better results.

Fixed Payments for Budgeting

Equipment loan payments are fixed—they never change. You know exactly what you’ll pay every month for the loan term. This makes budgeting and financial forecasting simple and reliable.

Contrast this with volatile operating costs or the uncertainty of leasing with potential renewal rate increases.

How to Get Equipment Financing with LendWiz

We’ve covered what equipment financing is and how it works. Now let’s walk through how LendWiz makes it easy to get the equipment financing your business needs.

The LendWiz Difference

LendWiz simplifies equipment financing through:

- No credit impact to apply. Check your prequalification without a hard credit pull.

- Fast approvals. Most qualifying applications get approved within 24-48 hours.

- Transparent pricing. No hidden fees or surprises. You get a complete breakdown upfront.

- Flexible terms. Choose loan terms from 24-84 months matched to your equipment and cash flow.

- Industry expertise. We understand equipment financing for restaurants, construction, trucking, manufacturing, and more.

- Direct funding. Quick funding so you get your equipment fast.

- Competitive rates. We work with our nationwide lender network to find the best rates for your situation.

The 3-Step Process

Step 1: Prequalify

Visit LendWiz.com and complete a quick prequalification form. You’ll get instant feedback on your approval odds and estimated rate range. No credit impact.

Step 2: Get Approved

After prequalification, we submit your full application. Our team reviews your details and gets you approved within 1-2 business days. You’ll receive a formal loan offer with all terms clearly stated.

Step 3: Get Funded & Receive Equipment

After you accept your offer and sign documents (all electronic), we fund your loan within 3-7 business days. You’ll receive your equipment quickly and start building your business.

What to Have Ready

To speed up the process, gather these documents before applying:

- Recent business and personal tax returns

- Last 2-3 months of business bank statements

- Business license or articles of incorporation

- Details about the equipment you want to purchase

- Equipment quotes or vendor information

Ready to move forward? Apply with LendWiz today.

Frequently Asked Questions

Can startups qualify for equipment financing?

Yes, though with limitations. Most lenders require 6-24 months in business. If your startup is newer, SBA loans and vendor financing are your best options. Equipment financing becomes easier once you’ve been operating 2+ years and can show revenue.

What credit score do I need for equipment financing?

You can qualify with a credit score as low as 580-600, though better rates come with scores of 650+. Equipment financing is more flexible than traditional bank loans because the equipment serves as collateral.

Can I finance used equipment?

Yes. Used equipment financing is common and often carries slightly higher rates than new equipment due to higher default risk. Get an independent appraisal to support the equipment’s value.

What equipment qualifies for financing?

Generally, any business asset with useful life beyond one year qualifies: machinery, trucks, POS systems, refrigeration, construction equipment, medical equipment, and more. Inventory, real estate, and intangible assets typically don’t qualify.

Is Section 179 deduction the same as depreciation?

No. Section 179 lets you deduct the full purchase price in year one (up to the annual limit). Depreciation spreads the deduction over several years. Section 179 is usually more beneficial because you deduct faster.

How long does equipment financing approval take?

Most lenders approve qualifying applications in 24-48 hours. Funding typically takes an additional 3-7 business days. SBA loans take longer—30-45 days—but offer better rates and longer terms.

Can I pay off equipment financing early?

Usually yes, though check your loan agreement for prepayment penalties. Many lenders allow early payoff without penalties, which saves you interest. Early payoff can make sense if you have extra cash.

What happens if I default on equipment financing?

If you miss payments, the lender can repossess the equipment. Repossession damages your credit and leaves you without the equipment. Contact your lender immediately if you’re struggling with payments—many lenders work with borrowers to modify terms or create payment plans.

Ready to Finance Your Equipment? Apply with LendWiz

You’ve learned what equipment financing is, how it works, what it costs, and how it compares to other options. Now it’s time to move forward.

Equipment financing gives you access to the tools your business needs without depleting your cash reserves. Whether you’re opening a restaurant, expanding your construction fleet, upgrading your manufacturing line, or launching any other equipment-dependent business, financing makes it possible.

Ready to get started?

- Visit LendWiz.com and complete our quick prequalification form

- Get instant feedback on your approval odds and estimated rates

- Submit your full application and get approved within 24-48 hours

- Sign documents electronically

- Receive funding and get your equipment

The right equipment drives business growth. Equipment financing makes that growth possible.